REV Group Reports Strong Q2 Results; Updates Guidance – RVBusiness – Breaking RV Industry News

- Second quarter net sales of $629.1 million compared to $616.9 million in the prior year quarter, the latter of which included $32.9 million related to the Bus Manufacturing Businesses1

- Excluding the impact of the Bus Manufacturing Businesses, net sales increased $45.1 million, or 7.7% compared to the prior year quarter

- Second quarter net income of $19.0 million compared to net income of $15.2 million in the prior year quarter

- Second quarter Adjusted EBITDA2 was $58.9 million compared to $37.5 million in the prior year quarter, the latter of which included $1.5 million related to Bus Manufacturing Businesses

- Excluding the impact of the Bus Manufacturing Businesses, Adjusted EBITDA increased $22.9 million, or 63.6% compared to the prior year quarter.

- Second quarter Adjusted Net Income2 of $35.4 million compared to $20.9 million in the prior year quarter

- The company repurchased approximately 2.9 million of its common shares for $88.4 million during the quarter, excluding commissions, fees, and excise taxes

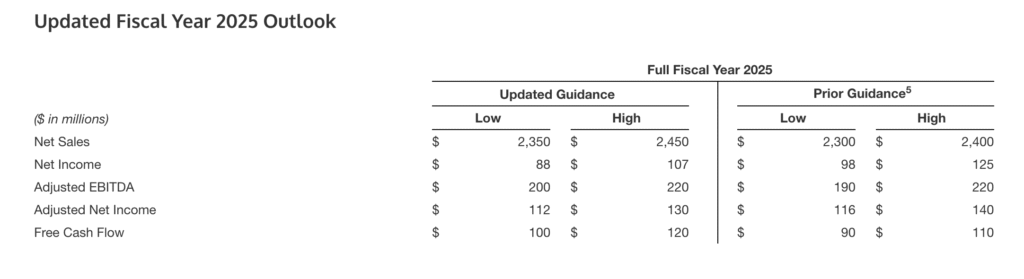

- Updated full-year fiscal 2025 outlook:

- Net sales of $2.35 to $2.45 billion, Net income of $88.0 to $107.0 million, Adjusted EBITDA of $200.0 to $220.0 million, Adjusted Net Income of $112.0 to $130.0 million, Net cash provided by operating activities of $150.0 to $165.0, and Free Cash Flow2 of $100.0 to $120.0 including capital expenditures of $45.0 to $50.0 million

BROOKFIELD, Wis. – REV Group, Inc. (NYSE: REVG), a manufacturer of industry-leading specialty and RVs, today (June 5) reported results for the three months ended April 30. Consolidated net sales in the second quarter 2025 were $629.1 million, compared to $616.9 million for the three months ended April 30, 2024. Net sales for the second quarter 2024 included $32.9 million attributable to the Bus Manufacturing Businesses. Excluding the impact of the Bus Manufacturing Businesses, net sales increased $45.1 million, or 7.7% compared to the prior year quarter. The increase, excluding the impact of the Bus Manufacturing Businesses, was primarily due to higher net sales in the Specialty Vehicles segment, partially offset by lower net sales in the Recreational Vehicles segment.

The company’s second quarter 2025 net income was $19.0 million, or $0.38 per diluted share, which included a net $13.4 million loss on assets held for sale after considering the related income tax benefit, compared to net income of $15.2 million, or $0.28 per diluted share, in the second quarter 2024. Adjusted Net Income for the second quarter 2025 was $35.4 million, or $0.70 per diluted share, compared to Adjusted Net Income of $20.9 million, or $0.39 per diluted share, in the second quarter 2024. Adjusted EBITDA in the second quarter 2025 was $58.9 million, compared to $37.5 million in the second quarter 2024. Adjusted EBITDA for the second quarter 2024 included $1.5 million attributable to Bus Manufacturing Businesses. Excluding the impact of the Bus Manufacturing Businesses, Adjusted EBITDA increased $22.9 million, or 63.6% compared to the prior year quarter. The increase, excluding the impact of the Bus Manufacturing Businesses, was primarily due to the higher contribution from the Specialty Vehicles segment and lower contribution from the Recreational Vehicles segment.

| _______________________________________ |

| 1 In fiscal 2024, the company exited bus manufacturing through the sale Collins Bus Corporation (“Collins”) in the first quarter, and El Dorado National (California), Inc (“ENC”) in the fourth quarter. Collins and ENC are collectively referred to as the “Bus Manufacturing Businesses”. |

| 2 REV Group, Inc. Adjusted Net Income, Adjusted EBITDA, and Free Cash Flow are non-GAAP measures that are reconciled to their nearest GAAP measure later in this release. |

“We are pleased that the second quarter’s performance continued to build upon our recent achievements. The standout this quarter was the sustained year-over-year increase in manufacturing throughput within the fire group, which played a pivotal role in driving our top-line growth,” REV Group Inc. President and CEO, Mark Skonieczny said. “Within the quarter we utilized our robust cash flow and financial position to repurchase $88 million of shares, which we view as an attractive use of capital. Building on the performance demonstrated through the first half of the fiscal year, we also plan to accelerate certain capital investments to further our manufacturing throughput goals including a $20 million investment in our Brandon, South Dakota location. Today we are updating our full year fiscal guidance with an expectation that year-to-date performance and sustained operational excellence provide a foundation to offset the potential impacts from tariffs.”

REV Group Second Quarter Segment Highlights

Specialty Vehicles Segment

Specialty Vehicles segment net sales were $453.9 million in the second quarter 2025, an increase of $16.5 million, or 3.8%, from $437.4 million in the second quarter 2024. Net sales for the second quarter 2024 included $32.9 million attributable to the Bus Manufacturing Businesses. Excluding the impact of the Bus Manufacturing Businesses, net sales increased $49.4 million, or 12.2% compared to the prior year quarter. The increase in net sales compared to the prior year quarter, excluding the impact of the Bus Manufacturing Businesses, was primarily due to increased shipments of fire apparatus and price realization, partially offset by an unfavorable mix of fire apparatus. Specialty Vehicles segment backlog at the end of the second quarter 2025 was $4,282.0 million compared to $4,064.4 million at the end of the second quarter 2024. Backlog at the end of the second quarter 2024 included $54.8 million related to the Bus Manufacturing Businesses. Excluding the impact of the Bus Manufacturing Businesses, backlog increased $272.4 million compared to the prior year quarter. The increase, excluding the impact of the Bus Manufacturing Businesses, was primarily due to continued demand and order intake for fire apparatus and ambulance units and pricing actions, partially offset by increased production and shipments of fire apparatus.

Specialty Vehicles segment Adjusted EBITDA was $56.3 million in the second quarter 2025, an increase of $22.5 million, or 66.6%, from Adjusted EBITDA of $33.8 million in the second quarter 2024. Adjusted EBITDA for the second quarter 2024 included $1.5 million attributable to the Bus Manufacturing Businesses. Excluding the impact of the Bus Manufacturing Businesses, Adjusted EBITDA increased $24.0 million, or 74.3% compared to the prior year quarter. Profitability within the segment, excluding the impact of the Bus Manufacturing Businesses, was primarily due to increased shipments of fire apparatus and price realization, partially offset by an unfavorable mix of fire apparatus and inflationary pressures.

Recreational Vehicles Segment

Recreational Vehicles segment net sales were $175.3 million in the second quarter 2025, a decrease of $4.4 million, or 2.4%, from $179.7 million in the second quarter 2024. The decrease in net sales compared to the prior year quarter was primarily due to lower unit shipments and increased dealer assistance, partially offset by pricing actions. Recreational Vehicles segment backlog at the end of the second quarter 2025 was $267.9 million, a decrease of $6.8 million compared to $274.7 million at the end of the second quarter 2024. The decrease was primarily the result of lower order intake in certain categories.

Recreational Vehicles segment Adjusted EBITDA was $10.9 million in the second quarter 2025, a decrease of $1.2 million, or 9.9%, from $12.1 million in the second quarter 2024. The decrease was primarily due to lower unit shipments and increased dealer assistance on certain models, partially offset by pricing actions and cost reduction initiatives.

Working Capital, Liquidity, and Capital Allocation

Net debt3 totaled $101.2 million as of April 30, 2025, including $28.8 million cash on hand. The company had $263.2 million available under its ABL revolving credit facility as of April 30, 2025, a decrease of $86.4 million compared to the October 30, 2024 availability of $349.6 million. On February 20, 2025, the Company amended its ABL Facility, extending the maturity, reducing the size of the facility and modifying certain terms. Details can be found in the Form 8-K filed on February 24, 2025.

During the second quarter 2025, the company repurchased approximately 2.9 million of its common shares for $88.4 million at an average purchase price of $30.70 per share, excluding commissions, fees and excise taxes. As of April 30, 2025, authorization to purchase approximately $142.4 million of shares remained under the current share repurchase program. Trade working capital4 for the company as of April 30, 2025 was $207.3 million, compared to $248.2 million as of October 30, 2024. The decrease was primarily due to the timing of accounts payable payments, lower inventory purchases, and higher receipts of customer advances, partially offset by the timing of accounts receivable collections. Capital expenditures in the second quarter 2025 were $11.4 million compared to $5.9 million in the second quarter 2024.

| _______________________________________ |

| 3 Net Debt is defined as total debt less cash and cash equivalents. |

| 4 Trade Working Capital is defined as accounts receivable plus inventories less accounts payable and customer advances. |

Quarterly Dividend

The company’s board of directors declared a regular quarterly cash dividend in the amount of $0.06 per share of common stock, payable on July 11, 2025, to shareholders of record on June 27, 2025, which equates to a rate of $0.24 per share of common stock on an annualized basis.

Click here for the full report.