Camping World Sees 3.6% Revenue Increase During Q1 – RVBusiness – Breaking RV Industry News

LINCOLNSHIRE, Ill. – Camping World Holdings, Inc. (NYSE: CWH), the World’s Largest Recreational Vehicle Dealer, on April 29 reported results for the first quarter ended March 31.

Marcus Lemonis, Chairman and Chief Executive Officer of CWH stated, “We made the commitment at the beginning of the year to sell more units and make more money. Our results reflect a material year-over-year improvement in adjusted EBITDA, increasing nearly 4x vs. the prior year, with another period of record new and used combined unit market share. We have not seen any discernable impacts on consumer behavior from tariffs, with our April-to-date same store unit sales tracking up mid-teens on used and up high-singles on new. Through recent actions to lower headcount and optimize our footprint, we expect SG&A reductions to further improve profitability in the months ahead.”

Matthew Wagner, President of CWH commented, “Our business continues to exhibit consistent growth in real time. We remain confident in our guideposts to deliver growth in excess of low-double digits in used units and low single digits in new units, vehicle gross margins within our historical range and SG&A as a percentage of gross profit improving by 600-700 basis points(1). We continue to meet the customer where they want to be met in terms of price and payment, leading to slightly lower than anticipated ASPs to start the year. We are rigorously managing our SG&A as we aim to mitigate any ASP or macroeconomic variability that could persist in the near-term.”

First Quarter-over-Quarter Operating Highlights

- Revenue was $1.4 billion for the first quarter, an increase of $49.5 million, or 3.6%.

- New vehicle revenue was $621.4 million for the first quarter, a decrease of $34.7 million, or 5.3%, and new vehicle unit sales were 16,726 units, a decrease of 156 units, or 0.9%. Used vehicle revenue was $422.4 million for the first quarter, an increase of $84.7 million, or 25.1%, and used vehicle unit sales were 13,939 units, an increase of 3,245 units, or 30.3%. Combined new and used vehicle unit sales were 30,665, an increase of 3,089 units, or 11.2%.

- Average selling price of new vehicles sold decreased 4.4% and average selling price of used vehicles sold decreased 4.0%.

- Same store new vehicle unit sales decreased 2.0% for the first quarter and same store used vehicle unit sales increased 28.5%. Combined same store new and used vehicle unit sales increased 9.8%.

- Products, service and other revenue was $165.0 million, a decrease of $12.9 million, or 7.3%, driven primarily by the divestiture of our RV furniture business in May 2024 and a reallocation of service labor toward used inventory reconditioning. Products, service and other gross margin was 48.6%, an increase of 580 basis points, driven by the divestiture of the RV furniture business, higher billing rates for service labor, and improved margins on our aftermarket part assortment.

- New vehicle gross margin was 13.7%, a decrease of 19 basis points, driven primarily by the 4.4% decrease in the average selling price per new vehicle sold, partially offset by a 4.2% reduction in the average cost per new vehicle sold. Used vehicle gross margin was 18.6%, an increase of 104 basis points, primarily due to a 5.3% decrease in the average cost per unit sold, partially offset by the 4.0% lower average selling price.

- Gross profit was $429.6 million, an increase of $27.2 million, or 6.8%, and total gross margin was 30.4%, an increase of 89 basis points. The gross profit increase was mainly driven by the $19.2 million higher used vehicle gross profit from the increase in used vehicle unit sales and gross margin as discussed above and $13.2 million higher finance and insurance, net (“F&I”) gross profit largely from the 11.2% increase in combined new and used vehicle unit sales and new F&I offerings. The gross margin improvements for used vehicles and products, service and other discussed above were partially offset by a 511 basis point decrease in Good Sam Services and Plans gross margin to 61.6%, which was primarily a result of higher roadside assistance claim costs.

- Selling, general and administrative expenses (“SG&A”) were $387.4 million, an increase of $16.0 million, or 4.3%. This increase was primarily driven by a $9.6 million increase in employee cash compensation costs, $7.3 million of additional advertising expenses, and a $2.0 million increase in employee stock-based compensation (“SBC”) expense, partially offset by $4.2 million of reduced legal fees. SG&A Excluding SBC(2)was $380.3 million, an increase of $13.9 million, or 3.8%.

- Floor plan interest expense was $18.3 million, a decrease of $9.6 million, or 34.3%, as a result of lower interest rates and lower principal balances. Other interest expense, net was $30.5 million, a decrease of $5.6 million, or 15.4%, as a result of lower interest rates and, to a lesser extent, lower principal balances.

- Net loss was $24.7 million for the first quarter of 2025, an improvement of $26.1 million, or 51.4%. Adjusted EBITDA(2)was $31.1 million, an increase of $22.9 million, or 278.0%.

- Diluted loss per share of Class A common stock was $(0.21), an improvement of $0.30, or 58.8%. Adjusted loss per share – diluted(2)of Class A common stock was $(0.16), an improvement of $0.24, or 60.0%.

- The total number of our store locations was 209 as of March 31, 2025, a net decrease of six store locations from March 31, 2024, or 2.8%.

(1) Refers to a comparison to the baseline of SG&A as a percentage of gross profit of 86.2% as calculated from the $1.6 billion SG&A and $1.8 billion total gross profit for the year ended December 31, 2024.

(2) Adjusted loss per share – diluted, Adjusted EBITDA, and SG&A Excluding SBC are non-GAAP measures. For a reconciliation of these non-GAAP measures to the most directly comparable GAAP measures, see the “Non-GAAP Financial Measures” section later in this press release.

Revisions to Prior Period Condensed Consolidated Financial Statements

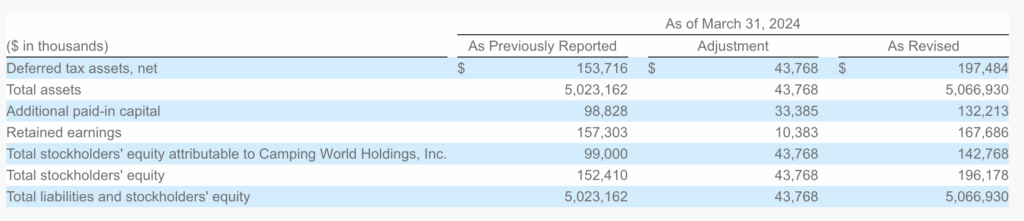

Subsequent to the issuance of the Company’s condensed consolidated financial statements for the quarter ended March 31, 2024, the Company’s management identified prior period misstatements related to the measurement of the realizable portion of the Company’s outside basis difference deferred tax asset in CWGS Enterprises, LLC (“CWGS, LLC”), including the associated valuation allowance. As a result, deferred tax assets, net, additional paid-in capital, and income tax benefit (expense) as of and for the years ended December 31, 2023 and 2022 were revised in the Company’s Annual Report on Form 10-K for the year ended December 31, 2024 filed with the SEC on February 28, 2025. The misstatements impacted the beginning balances of deferred taxes, net, additional paid-in capital, and retained earnings, which have been revised from the amounts previously reported as of March 31, 2024. The Company evaluated the materiality of these errors, both qualitatively and quantitatively, and determined the effect of these revisions was not material to the previously issued financial statements.

The following table presents the effect of the immaterial misstatements on the Company’s consolidated balance sheet for the period indicated:

Earnings Conference Call and Webcast Information

A conference call to discuss the Company’s first quarter 2025 financial results is scheduled for April 30, 2025, at 7:30 am Central Time. Investors and analysts can participate on the conference call by dialing 1-844-826-3035 (international callers please dial 1-412-317-5195) and using conference ID# 10199179. Interested parties can also listen to a live webcast or replay of the conference call by logging on to the Investor Relations section on the Company’s website at http://investor.campingworld.com. The replay of the conference call webcast will be available on the investor relations website for approximately 90 days.

Presentation

This press release presents historical results for the periods presented for the Company and its subsidiaries, which are presented in accordance with accounting principles generally accepted in the United States (“GAAP”), unless noted as a non-GAAP financial measure. The Company is the sole managing member of CWGS, LLC, with sole voting power in and control of the management of CWGS, LLC. As of March 31, 2025, the Company owned 61.1% of CWGS, LLC. Accordingly, the Company consolidates the financial results of CWGS, LLC and reports a non-controlling interest in its consolidated financial statements. Unless otherwise indicated, all financial comparisons in this press release compare our financial results for the first quarter ended March 31, 2025 to our financial results from the first quarter ended March 31, 2024.