Despite RV Headwinds, Myers Industries Posts Positive Q3 – RVBusiness – Breaking RV Industry News

AKRON, Ohio – Myers Industries Inc. (NYSE: MYE), the parent company of Ameri-Kart and Elkhart Plastics and a leading manufacturer of a wide range of polymer and metal products and distributor for tire, wheel, and under vehicle service industry, today announced results for the third quarter ended Sept. 30, 2024.

Third Quarter 2024 Financial Highlights

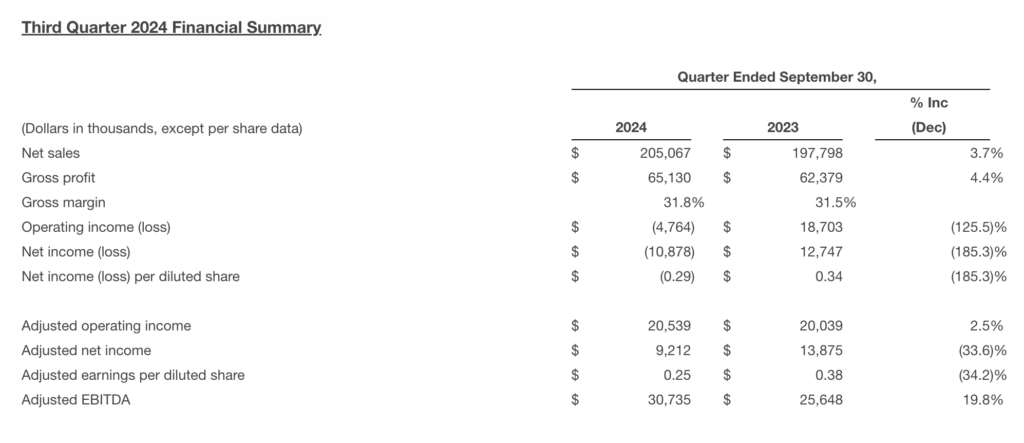

- Net sales of $205.1 million compared with $197.8 million in the prior-year period

- Net Income (loss) of $(10.9) million, compared to $12.7 million in the prior-year period inclusive of a non-cash goodwill impairment charge of $22.0 million

- Adjusted EBITDA of $30.7 million, compared to $25.6 million in the prior-year period

- GAAP gross margin of 31.8%, up 30 basis points versus the prior-year period

- Adjusted gross margin of 32.4%, up 70 basis points versus the prior-year period

- GAAP net income (loss) per diluted share of $(0.29) compared with $0.34 in the prior-year period

- Adjusted earnings per diluted share of $0.25 compared with $0.38 in the prior-year period

- Cash flow provided by operations of $17.3 million and free cash flow of $10.1 million

- Additional debt paydown of $13 million

Dave Basque, Myers Industries interim president and CEO, stated in a release: “This quarter’s results were driven by continued strong performance from our Signature Systems acquisition, growth in our military end market, the initial benefits of our cost cutting initiatives and reduced variable compensation. These benefits mitigated some broader macro-economic challenges in the RV and Marine and new headwinds in the Food and Beverage end markets.

“During the quarter, we diligently focused on our cost containment actions which we now estimate will lead to an additional $15 million in annualized cost savings. These cost savings are incremental to our original target of $7 million to $9 million and are expected to be driven by labor savings, manufacturing efficiencies, continued footprint optimization and other savings initiatives. We will continue to implement cost actions to help mitigate the impact of revenue headwinds in key end markets.

“We have taken additional action to address the underperformance of our Distribution business, starting with naming Jeff Baker as President, Distribution. Since assuming this role on Sept. 30, Jeff and his team have systematically identified plans to close sales coverage gaps and win back customers, add digital sales channels, improve the customer experience and implement further efficiency improvements.

“We are updating our outlook and expect full year adjusted earnings per share to be in the range of $0.92 to $1.02. We continue to have confidence in the growth and earnings potential of our four power brands as demand recovers in affected end markets, and we remain focused on improving operations in the near-term to navigate choppy macro-economic conditions.”

Net sales were $205.1 million, an increase of $7.3 million, or 3.7%, compared with $197.8 million for the third quarter of 2023. The increase in net sales was driven by contributions from the recent acquisition of Signature Systems, partially offset by lower volumes and pricing in both the Material Handling and Distribution segments.

Gross profit increased $2.8 million, or 4.4%, to $65.1 million, driven by performance at Signature Systems and favorable product mix, partially offset by lower pricing and volume, as well as higher material and other cost inflation. Gross margin improved 30 basis points to 31.8% compared with 31.5% for the third quarter of 2023. On an adjusted basis, gross margin increased 70 basis points to 32.4% from 31.7%. Selling, general and administrative expenses were $47.7 million, an increase of $4.0 million, primarily due to the addition of Signature and partially offset by lower incentive compensation expense. SG&A as a percent of sales was 23.3% vs 22.1% in the prior year in part due to the executive severance recorded in the quarter. The company also recorded a $22.0 million non-cash goodwill impairment charge related to goodwill from prior rotational molding acquisitions. Net income per diluted share was ($0.29), compared with $0.34 for the third quarter of 2023. Adjusted earnings per diluted share were $0.25, compared with $0.38 for the third quarter of 2023.

Third Quarter 2024 Segment Results

(Dollar amounts in the segment tables below are reported in millions)

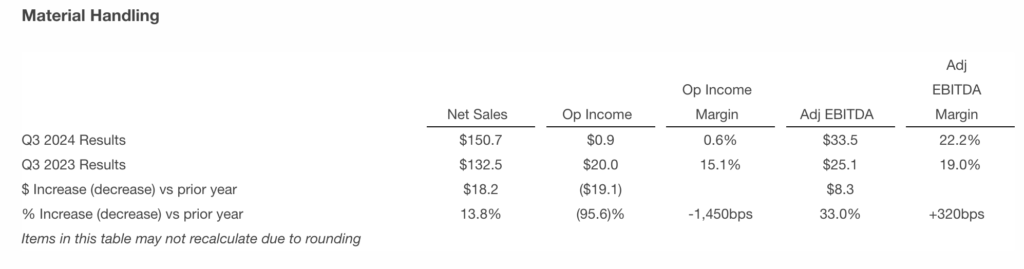

Net sales for the Material Handling segment were $150.7 million, an increase of $18.2 million, or 13.8%, compared with $132.5 million for the third quarter of 2023. Sales from the addition of Signature Systems were partly offset by sales declines, primarily in Seed boxes and within Food and Beverage end markets.

Operating income was $0.9 million compared with $20.0 million in the third quarter of 2023 primarily due to the non-cash goodwill impairment and the lower sales volume and pricing in the legacy business, partially offset by the Signature acquisition. Material Handling’s operating income margin of 0.6%, or 15.2% excluding the non-cash goodwill impairment, compared to 15.1% in the third quarter of 2023. Adjusted EBITDA increased 33.0% to $33.5 million, compared with $25.1 million in the third quarter of 2023. SG&A expenses increased year-over-year, primarily due to incremental SG&A from Signature, partly offset by lower incentive compensation. Adjusted EBITDA margin improved by 320 basis points, primarily attributed to the Signature acquisition, partially offset by higher material costs and lower sales volume and pricing in the legacy business. A $22.0 million non-cash goodwill impairment charge is included in the third quarter 2024 GAAP results of the Material Handling segment.

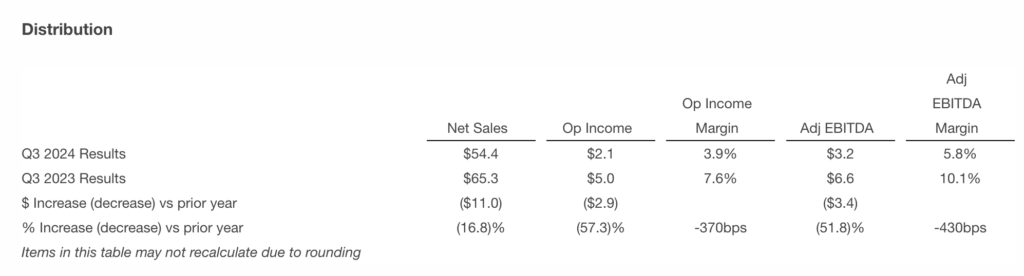

Net sales for the Distribution segment were $54.4 million, a decrease of $11.0 million, or 16.8%, compared with $65.3 million for the third quarter of 2023. The decrease was primarily driven by lower volume and pricing, partially offset by improved SG&A costs.

Operating income decreased $2.9 million to $2.1 million, compared with $5.0 million for the third quarter of 2023. Adjusted EBITDA decreased to $3.2 million, compared with $6.6 million in the third quarter of 2023. The decrease in operating income and adjusted EBITDA was primarily due to lower volume and pricing, as well as higher material costs. SG&A expenses decreased year-over-year, primarily due to lower payroll costs. The Distribution segment’s operating income margin was 3.9% compared with 7.6% for the third quarter of 2023. The Distribution segment’s adjusted EBITDA margin was 5.8%, compared with 10.1% for the third quarter of 2023.

Balance Sheet & Cash Flow

As of September 30, 2024, the Company’s cash on hand totaled $29.7 million. Total debt as of September 30, 2024, was $396.2 million. Under the terms of the Company’s loan agreement, its net leverage ratio was 2.7x and it had $239.4 million of availability under its revolving credit facility as of September 30, 2024. For the third quarter of 2024, cash flow provided by operations was $17.3 million and free cash flow was $10.1 million, compared with cash flow provided by operations of $22.1 million and free cash flow of $18.1 million for the third quarter of 2023. The decrease in free cash flow was driven primarily by the timing of disbursements. Capital expenditures for the third quarter of 2024 were $7.2 million compared with $4.1 million for the third quarter of 2023.

2024 Outlook

Based on current exchange rates, market outlook and business forecast, the Company is providing the following outlook for fiscal 2024:

- Net sales growth of 0% to 5% compared to prior guidance of 5% to 10%

- Net income per diluted share in the range of $0.11 to $0.21 compared to prior guidance of $0.76 to $0.91

- Adjusted earnings per diluted share in the range of $0.92 to $1.02 compared to prior guidance of $1.05 to $1.20

- Capital expenditures in the range of $28 million to $32 million compared to prior guidance of $30 million to $35 million

- Effective tax rate to approximate 26%

Myers will continue to monitor market conditions and provide updates throughout the year.