THOR Industries Q4 Shows ‘Strong Margin Performance’ – RVBusiness – Breaking RV Industry News

ELKHART, Ind., – THOR Industries, Inc. (NYSE: THO) today (Sept. 24) announced financial results for its fourth fiscal quarter ended July 31.

“Our teams delivered solid performances as we continue to navigate the persistent challenges in the industry’s retail environment. We realized strong margin performance relative to the current market conditions as our teams executed on strategic initiatives designed to maximize our operational efficiency. This long-term focus puts THOR in a strong position for our Fall Open House event and the coming winter season,” offered Bob Martin, President and CEO of THOR Industries.

“The macroeconomic challenges facing our independent dealers and end consumers have been an impediment to our industry for an extended period of time. THOR’s business model and discipline allow us to not just adjust to what we’ve referred to as ‘bouncing along the bottom,’ but to also make internal efficiency improvements which contributed to improving our fourth quarter gross profit margin despite the reduction in our net sales. While challenges persist, we are confident in our ability to continue to successfully manage our way through them. We will remain disciplined with production to help our independent dealer inventories stay fresh and in line with retail demand to protect margins in this challenging market. Our 44-year history has taught us that this cautious approach is healthy for our independent dealers, the industry and for THOR. Our confidence in the inevitable return of a robust market remains unchanged. It’s not an ‘if’ proposition but a ‘when’ proposition,” added Martin.

Fourth Quarter Financial Results

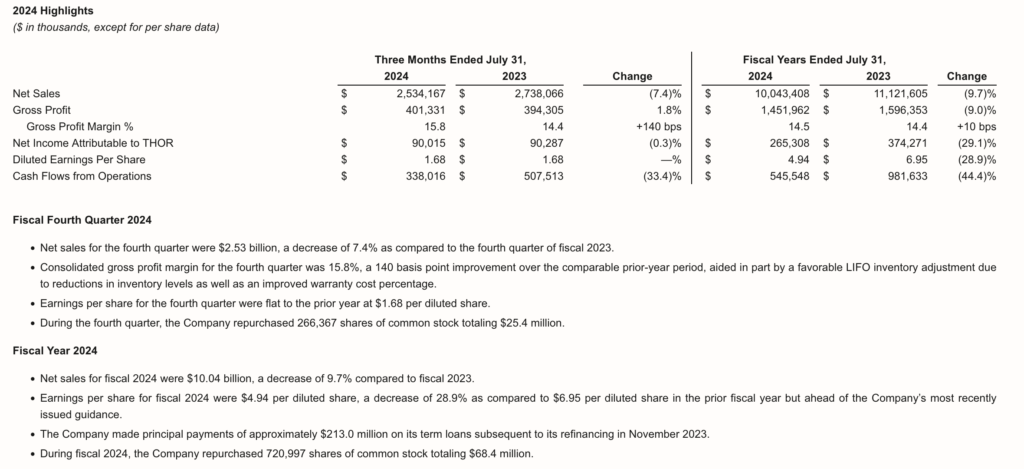

Consolidated net sales were $2.53 billion in the fourth quarter of fiscal 2024, compared to $2.74 billion for the fourth quarter of fiscal 2023.

Consolidated gross profit margin for the fourth quarter of fiscal 2024 was 15.8%, an increase of 140 basis points when compared to the fourth quarter of fiscal 2023, aided in part by a favorable LIFO inventory adjustment due to reductions in inventory levels as well as an improved warranty cost percentage.

Net income attributable to THOR Industries, Inc. and diluted earnings per share for the fourth quarter of fiscal 2024 were $90.0 million and $1.68, respectively, compared to $90.3 million and $1.68, respectively, for the fourth quarter of fiscal 2023.

THOR’s consolidated results were primarily driven by the results of its individual reportable segments as noted below.

Segment Results

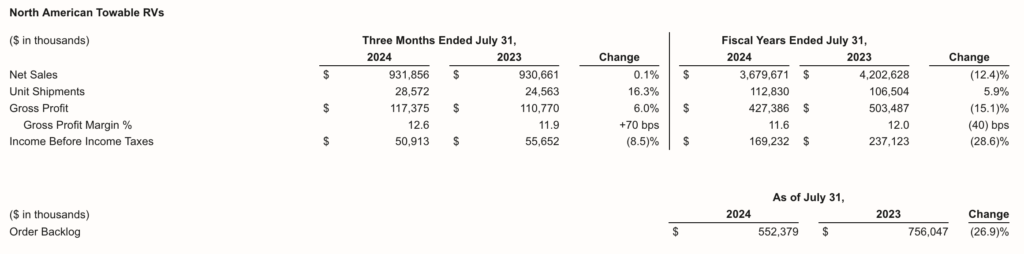

North American Towable RVs

- North American Towable RV net sales were up 0.1% for the fourth quarter of fiscal 2024 compared to the prior-year period, driven by a 16.3% increase in unit shipments offset by a 16.2% decrease in the overall net price per unit. The decrease in the overall net price per unit was primarily due to the combined impact of a shift in product mix toward our lower-cost travel trailers along with sales price reductions compared to the prior-year period.

- North American Towable RV gross profit margin was 12.6% for the fourth quarter of fiscal 2024, compared to 11.9% in the prior-year period. The increase in gross profit margin percentage was primarily due to a decrease in both the overhead and warranty expense percentages.

- North American Towable RV income before income taxes for the fourth quarter of fiscal 2024 was $50.9 million, compared to $55.7 million in the fourth quarter of fiscal 2023. This decrease was driven primarily by an increase in selling, general and administrative costs.

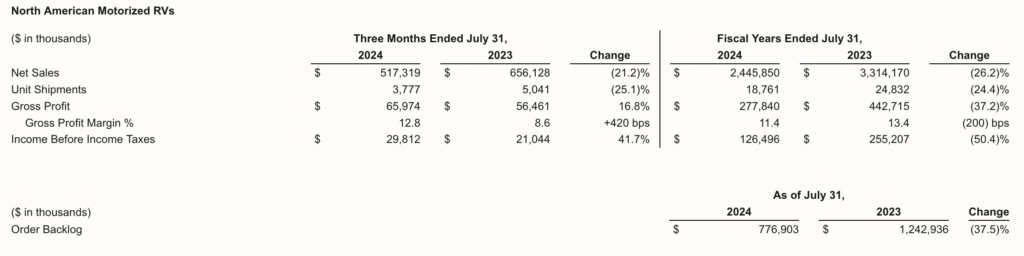

North American Motorized RVs

- North American Motorized RV net sales decreased 21.2% for the fourth quarter of fiscal 2024 compared to the prior-year period. The decrease was primarily due to a 25.1% reduction in unit shipments, as current dealer and consumer demand has softened in comparison to the prior-year period, partially offset by a 3.9% increase in net price per unit.

- North American Motorized RV gross profit margin was 12.8% for the fourth quarter of fiscal 2024, compared to 8.6% in the prior-year period. The increase in the gross profit margin percentage for the fourth quarter of fiscal 2024 was primarily driven by decreases in each of the material, labor and warranty cost percentages, with the decrease in material percentage largely due to the favorable impact of a LIFO inventory adjustment as a result of inventory reduction measures, partially offset by higher sales discounts.

- North American Motorized RV income before income taxes for the fourth quarter of fiscal 2024 increased to $29.8 million compared to $21.0 million in the prior-year period, driven by the increase in gross profit margin percentage.

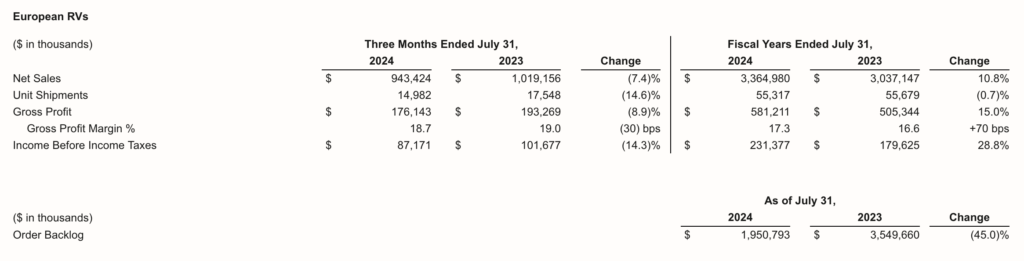

European RVs

- European RV net sales decreased 7.4% for the fourth quarter of fiscal 2024 compared to the prior-year period, driven by a 14.6% decrease in unit shipments offset in part by a 7.2% increase in the overall net price per unit due to the total combined impact of changes in product mix and price. The overall increase in net price per unit of 7.2% includes a 1.0% decrease due to the impact from foreign currency exchange rate changes.

- European RV gross profit margin was 18.7% of net sales for the fourth quarter of fiscal 2024 compared to 19.0% in the prior-year period, primarily due to slight increases in material and overhead cost percentages due to increased sales discounting, partially offset by an improved direct labor percentage.

- European RV income before income taxes for the fourth quarter of fiscal 2024 was $87.2 million compared to $101.7 million during the fourth quarter of fiscal 2023, with the decrease driven primarily by the decreased net sales and increased sales discounting compared to the prior-year period.

Management Commentary

“Our performance during the fourth quarter of our fiscal year 2024 was marked by a strong margin performance relative to current market conditions, as we saw an improvement in our gross margin percentage of 140 basis points over the fourth quarter of fiscal year 2023. The drivers for this improvement include our success in managing cost inputs, reduced warranty costs, optimizing our production processes and remaining disciplined with our production and inventory levels, as the reduction in inventories during the fourth quarter generated a favorable LIFO inventory adjustment. Our bottom line benefited from our successful execution of these strategies, as we saw our fourth quarter net income before income taxes as a percentage of sales increase 20 basis points compared to the prior-year period despite a 7.4% reduction in our consolidated net sales. For the full fiscal year, our top line declined by 9.7% while our gross profit margin percentage improved 10 basis points. Our focus in the current market is to continue to improve what we can control and to maximize our performance,” said Todd Woelfer, Senior Vice President and Chief Operating Officer.

“Given the current market environment, we were pleased with our fourth quarter performance. In our North American Towable segment, we saw flat net sales in our fourth quarter of fiscal year 2024 when compared to the fourth quarter of fiscal year 2023 but improved gross profit margin by 70 basis points on a similar sales volume. During the fourth quarter of fiscal year 2024, our Towable unit volumes increased by over 16% when compared to the prior-year fourth quarter as consumers continued to manifest a strong desire for the RV lifestyle despite macroeconomic conditions, albeit in smaller, more moderately-priced units. During the quarter, our warranty expense improved as we continued to focus on quality initiatives across the organization. In our North American Motorized segment, we saw sales drop over 21% when compared to the same period from the prior year. Affordability continues to be a challenge in the motorized segment as consumers navigate the current economic cycle. Despite the challenges at the retail and wholesale levels, we continue to improve our material, labor and employee benefit costs as well as our warranty costs which contributed to our gross profit margin improvement. Our North American Motorized segment gross profit margin percentage also benefited from the favorable impact of a LIFO inventory adjustment as a result of inventory reduction measures,” offered Woelfer.

“Down markets like the one we are currently experiencing in North America provide a great reconfirmation of our variable operating model. As it has consistently proven through such shifting cycles, our operating model is once again establishing itself to be ideal for our business. Unlike prior down cycles, we are experiencing in this down cycle the benefits of long-term strategic initiatives designed to drive stronger margins even in challenging conditions. These strategies include our disciplined production planning, our continued efforts to maximize operating efficiencies as we leverage our variable cost model, and our steadfast focus on improved quality. During the fiscal fourth quarter, we managed to have flat year-over-year diluted EPS performance despite a reduction in our consolidated top line of 7.4%. As we look ahead, we will continue to execute strategic initiatives designed to drive margin improvement while also working to best position our products to realize relative retail success in current market conditions,” added Woelfer.

“In our fourth quarter, our European team outperformed expectations. We have reported publicly that the benefit of dealer restocking that was realized over the first half of fiscal 2024 would dissipate in the latter half of the fiscal year. Our European segment generated gross profit margin of 18.7%, down just 30 basis points from the same period last year despite a top line decrease of 7.4% which was largely attributable to the moderation and then completion of the restocking cycle with European independent dealers. As we have reported previously, our European management team has improved the institutional margin profile of our European business such that, relative to any given market condition, our European operations will outpace historical gross profit margin performance in similar market conditions. Importantly, our European operation has grown its market share for the six months ended June 30, 2024, adding 3.5% of total market share year over year and becoming the overall European market leader. Fiscal year 2024 was another strong year for our European operation as our strategy to create geographic diversification continues to drive value,” explained Woelfer.

“During the quarter, we generated approximately $338.0 million of cash from operations, and for the full fiscal year, we generated approximately $545.5 million. As we’ve outlined in the past, we take a balanced approach to capital allocation. That was evident again this year as we returned earnings to shareholders through dividends, made significant payments on our debt, supported capital expenditures and repurchased shares of THOR stock,” added Colleen Zuhl, Senior Vice President and CFO.

“We paid down approximately $116.8 million in total debt during the fourth quarter. During the full fiscal year, we paid down approximately $224.2 million in total debt, including principal payments of approximately $213.0 million on our term loans subsequent to our November 2023 debt modification, along with approximately $11.2 million in payments related to our other debt facilities. Additionally, during fiscal 2024, we both extended the maturities on our Term Loan B and Asset Based Loan facilities and lowered the interest rates on our USD and Euro term loans.

“During the quarter we also repurchased 266,367 shares of our outstanding stock for $25.4 million, bringing our full fiscal year total stock repurchases to 720,997 shares for $68.4 million.

“Capital expenditures in the fourth fiscal quarter totaled $33.6 million, bringing our total for fiscal year 2024 to approximately $139.6 million, well under our original capital expenditure plan as we adjusted non-critical spend due to market conditions.

“Our liquidity remains a unique strength within the industry. On July 31, 2024, we had liquidity of approximately $1.32 billion, including approximately $501.3 million in cash on hand and approximately $814.0 million available under our asset-based revolving credit facility. As we continue to navigate a challenging and dynamic market, our financial strength, robust cash generation profile and balanced approach to capital allocation continues to provide us the ability to execute on our long-term strategic plan,” said Zuhl.

Outlook

“Our fiscal 2024 was a year in which many of our strategic initiatives favorably impacted our performance in a difficult market. Our choice to remain prudent through the soft North American market has translated to better consolidated margin performance. The talk of a softer market is beginning to sound like a broken record, but we remained focused on managing through it with increasing efficiency. The strength of THOR, founded in our operating companies’ outstanding and experienced teams and the well-known brands they provide to the market, is our strong balance sheet and robust independent dealer relationships. These differentiate us from our competition as our ability to manage through extended retail downturns is unmatched. As we exit our fiscal 2024 and begin our fiscal 2025, we remain mindful that our focus is to continue to improve how we operate the Company in not only the current cycle but also prepare ourselves for the robust market that we all know to be on the horizon,” said Martin.

“Our current view of fiscal year 2025 is in line with the recent RVIA industry-wide forecast which projected approximately 324,100 wholesale unit shipments for calendar 2024 and 346,100 unit shipments at the median of its range for calendar 2025. We believe the RVIA forecast for calendar 2025 is slightly aggressive and see potential for a range closer to 335,000 units. Our base assumption for forecasting will be that the macro challenges will persist through our fiscal year 2025, which runs from August 1, 2024 through July 31, 2025. In North America, we expect discounting in fiscal 2025 to remain elevated in our Motorized segment, while we expect discounts to slightly moderate in our Towable segment. In Europe, as we have exhausted the dealer restocking opportunity fully, we expect fiscal 2025 to present more challenges at both the top line and the gross profit margin line when compared to the record results of our European segment in fiscal 2024,” added Woelfer.

“Although the near-term environment remains challenging, we continue to be very optimistic about global consumer interest in the RV lifestyle and long-term demand for our products. We remain confident that our strong financial position and status as the global leader in the RV industry enables THOR to meet the challenges of the current market and positions the Company for success in the longer term,” Martin concluded.

Fiscal 2025 Guidance

“In planning for our fiscal year 2025, we anticipate that the RV market will continue to be challenging throughout our fiscal year which ends on July 31, 2025. While we acknowledge that a positive inflection in the macroeconomic conditions could occur before the end of our fiscal year 2025 that could favorably impact our financial performance, we do not currently model such an inflection beyond the normal seasonal lift we anticipate in the spring. As mentioned above, we anticipate that we will face market headwinds that will impact our full-year performance in both our North American Motorized and European segments. With a bias towards being conservative, the Company continues to be cautious on the global economic outlook and associated impacts on consumer demand and appetite for sizeable discretionary purchases. In Europe, we anticipate a reduction in our European segment net sales in fiscal 2025 compared to their record sales in fiscal 2024, which included restocking European independent dealer lots back to normalized levels. In North America, the Company’s operating plan for fiscal 2025 reflects an industry wholesale shipment range of between 330,000 and 345,000 units with wholesale shipments matching retail demand in total, but we are expecting that dealers will hold off as long as possible on stocking for the spring selling season to keep inventory levels low over the winter months. As we forecast the continuation of the softer market in fiscal year 2025, we will continue to manage the Company to maximize our performance in the current environment as we position products in the market that address the affordability concerns of independent dealers and consumers and continue to lower the average sales price of our units. Given our expectations surrounding overall market volumes in both North America and Europe, the Company is introducing its initial guidance for fiscal 2025,” commented Woelfer.

For fiscal 2025, the Company’s full-year guidance includes:

- Consolidated net sales in the range of $9.0 billion to $9.8 billion

- Consolidated gross profit margin in the range of 14.7% to 15.2%

- Diluted earnings per share in the range of $4.00 to $5.00

“As we look beyond our fiscal 2025, we expect to see a stronger retail environment in the latter half of calendar 2025 and the beginning of our fiscal 2026. Our operating companies are well positioned to leverage the capacity of THOR to realize the financial benefits of the coming return of a robust retail environment. We anticipate that in a more robust retail environment, THOR will seize market share and meaningfully grow diluted EPS as it has after previous down cycles,” concluded Woelfer.

Supplemental Earnings Release Materials

THOR Industries has provided a comprehensive question and answer document, as well as a PowerPoint presentation, relating to its quarterly results and other topics.

To view these materials, go to http://ir.thorindustries.com.